Many savvy investors investigate balance sheets to determine what are retained earnings. This is because the balance sheet tells a story of the entire history of the company. It reflects cumulative values since the inception of the company. Specifically, the retained earnings balance sheet account represents the cumulative net earnings since the company started.

It is important to understand what are retained earnings and what the information means if you are looking to invest in a company. Retained earnings are one of the things Warren Buffett looks at when he determines which company is worth investing in. It tells a story. Learn what a story it tells and why the story is important. Also, learn how to calculate it when it is not apparent on the balance sheet.

What Are Retained Earnings?

What are retained earnings? Retained earnings are classified as equity on the balance sheet. Balance sheet items are represented as the sum value since the inception of the company. Balance sheet reports are typically run monthly, quarterly and annually. Retained earnings represent the net of all net income, both positive and negative (net profit and a net loss) and all dividends paid. This is also known as accumulated earnings, retained capital or earned surplus.

Tax Implications

Knowing what are retained earnings is very important for taxes. Most companies, barring nonprofits, are subject to a corporate tax on their net income for the fiscal year. This can be any 12-month period, but often runs from January to December or July to June. Retained earnings represent net income after tax. Most jurisdictions state no tax is payable on the accumulated earnings retained by a company, creating the potential for tax avoidance. Tax avoidance is legally using tax law to your advantage to reduce the amount of tax you are liable to pay. This differs from tax sheltering, which is not always legal.

In this case, some high-income taxpayers “park” income inside a private company rather than being paid out as dividends and taxed at the individual income rates. To combat this, some jurisdictions enact an undistributed profits tax on retained earnings of private companies. This is often at the highest individual marginal tax rate.

Most jurisdictions will not treat the issuance of bonus shares as a dividend distribution even if it is funded from retained earnings. This is not a taxable event for the shareholder as it is not recognized until it is sold. Retained earnings increase a shareholder equity which increases the value of each shareholder’s stock. If the shares are worth more when sold than the original purchase price, the stock owner must pay capital gains on the profits.

The term ‘Short-term capital gains,’ refers to personal profits from a sale when a share was held for up to 12 months. These are taxed at the ordinary income rate. Long-term capital gains are taxed at a much lower rate to encourage long-term investing and are derived from profits gained on the sale of appreciated shares held for longer than 12 months. Depending on your ordinary income tax bracket, you may not owe any money on your long-term capital gains.

Why Is It Important to Understand?

It is important to understand what are retained earnings. If you are investing in a company, retained earnings can indicate to you a company’s decision to pay profits out to stakeholders or reinvest them in the business, be it assets (purchasing equipment), liability reduction (paying off high-interest debt) or investing in research and development for a profitable business venture in an expanding market.

It is difficult to compare retained earnings from company to company. Older companies of the same size in the same industry may have much higher retained earnings than a newer comparable company due to having greater profits over time. However, since the balance sheet reflects net values since inception, an older company would have several more years of net profits to reflect in their retained earnings account.

Perhaps the most common analysis performed on the retained earnings account involves comparing the retained earnings per share to the profit per share over a specific period, usually quarterly and annually. You can also analyze the amount of capital retained to the change in share price during a specific time. Capital refers to anything used to generate income. Warren Buffett, one of the world’s most prominent value investors, developed look-through earnings which are a method that accounts for taxes.

Capital-intensive and growing industries usually retain more of their earnings because they require more asset investment to operate. These include automobile manufacturing, telecommunications, and transportation sectors. Car manufacturers have the initial capital cost of assets such as machines to do some work. However, they also have to invest in human capital. Remember, capital refers to anything used to generate income. It takes people to generate earnings for a company as well. This is all important when understanding what are retained earnings.

How Do You Calculate Retained Earnings?

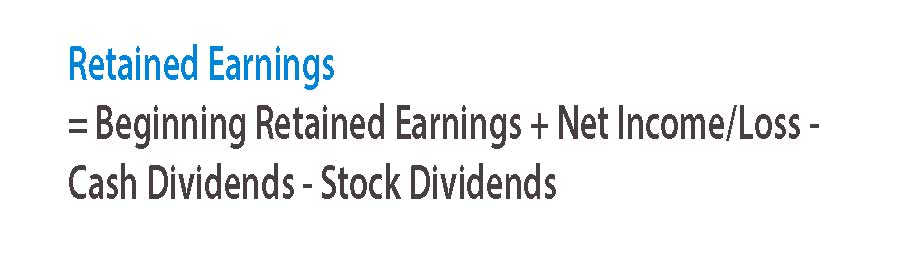

What are retained earnings formula components? The retained earnings calculation involves a formula that gets the balance in the retained earnings account at the end of a reporting period. To calculate the retained earnings balance for the period, start with the beginning retained earnings. This should be the same as the ending retained earnings of the last period. Add the net income earned during this period and subtract any dividends paid. This will get you the ending retained earnings balance.

The only reason a company’s beginning retained earnings balance would change is if it had to retroactively change its financial statements due to a change in accounting principle. For example, Netflix had to revise their financial statements after auditors determined they were not aggressive enough in the amortization of production costs.

It is possible for a company to have negative retained earnings. This can occur when the company owes more to shareholders in dividends than is in their retained earnings balance. It can also occur if a company retroactively had to reclassify assets as expenses. This would have reduced their net income, so the effect you see in the general ledger and on the balance sheet is a reduction to assets and a reduction to retained earnings. This is because net income flows to retained earnings, but the books cannot be changed once they are closed.

Having money in your retained earnings account does not mean you will distribute the money to shareholders. This is particularly true if a company has profitable business ventures to invest in. This is usually the case in an expanding market. As all revenues and expenses impact the net income portion of the retained earnings formula, a company’s retained earnings change nearly daily.

I Don’t See R/E on the Balance Sheet

Sometimes, retained earnings are not included on the balance sheet. To derive it from the information you have, you need to understand the basic accounting principle. It states: assets = liabilities + shareholder’s equity. Subtract liabilities from assets to solve for a shareholder’s equity. If you know only retained earnings and common stock make up shareholder’s equity, subtract the common stock line item on the balance sheet from shareholder equity to solve for retained earnings.

Similarly, if more accounts make up equity, subtract them out until you get to only retained earnings. Recall that assets = liabilities + equity. If you see a trust or mutual fund on the asset portion of the balance sheet, you know that account is represented on the equity side of the balance sheet.

Conclusion

Retained earnings, also known as cumulative earnings, is a balance sheet account. Balances on the balance sheet reflect the net value of the balance since the inception of the business. The basic accounting principle is assets equal the sum of liabilities and equity. Even if retained earnings are not specifically stated on a company’s balance sheet, it is simple to calculate what are retained earnings. Subtract total liabilities from total assets to get shareholder equity. From shareholder equity, subtract common stock and any other equity account other than retained earnings.

To calculate what are retained earnings for the end of a period, take the beginning balance of retained earnings for the period, subtract any dividends paid and add the net profit or subtract the net loss for the period. Since revenue and expenses affect the P&L which affects net income which affects retained earnings, the balance of this account changes nearly daily.

Retained earnings tell a story. They tell the story of what a company does with its profits. A company can either pay their profits out to shareholders in the form of dividends or reinvest the profits back into profitable business ventures. This is especially true in growing or capital-intensive industries like the automobile manufacturing industry, the transportation sector, and telecommunications. There are heavy asset investment requirements to operate in these industries. Capital refers to anything necessary to generate income from land to infrastructure to equipment to people.

It is possible to have negative retained earnings. This means that since the beginning of the company there have been more dividends paid out than profits earned. It is difficult to compare retained earnings from company to company. Since it is a cumulative number, older companies likely have much higher retained earnings account balance as they have had more years to accumulate net profits.